The Commercial Experience 21.03 -

The great re-opening, Afterpay Ads, equine fringe theories and why the March quarter for advertising is shaping up to be the biggest in a long time.

Week 3, edition 3. Thanks to everyone who is reading, writing feedback, and sharing with friends and colleagues. Keep the feedback coming and if there’s anything you’d like to see in TCE in the future - hit me up!

This week takes a few twists and turns. Vaccination, re-opening, buy now pay later and predictions for a big advertising boom to begin 2022.

What’s the deal with the fringe thinking that taking an equine parasite drug is a better way to prevent COVID than taking a vaccine?

Last week the CDC in the United States needed to release formal guidance on the dangers of taking Ivermectin to either prevent of treat COVID. In a nutshell, hospitals had reported a rush in poisoning due to patients reporting after taking Ivermectin as a result of it being promoted in elements of the media and the web.

Fox News has been giving oxygen to the theory - Fox News: Biologist to Tucker: If Ivermectin proven effective against COVID, it moots vaccine push - and it’s gaining a lot of traction on social media.

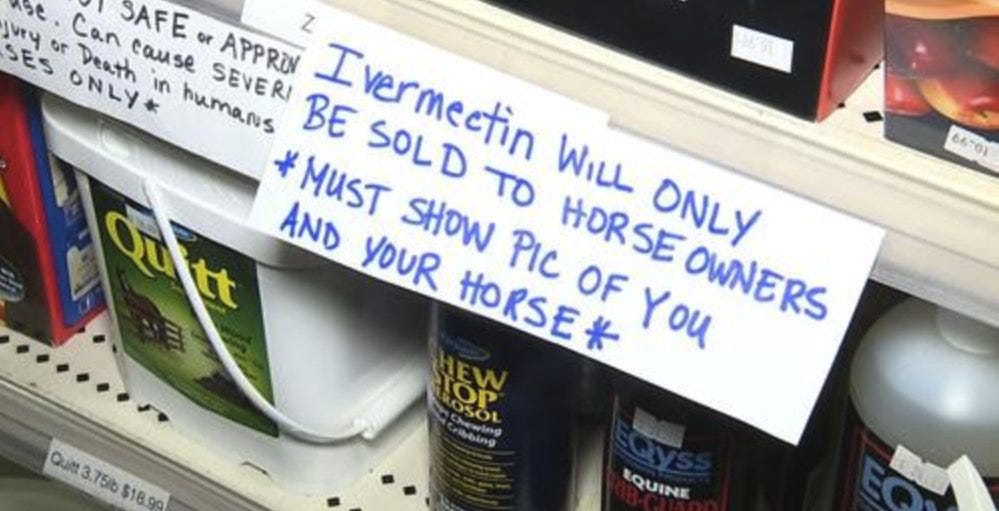

For instance, check this wild thread. Those who have taken the drug have reported soiling themselves in public … and if that wasn’t enough to stop, they are then being egged on by other users to keep going. A lot of those wanting to trial the drug are buying Ivermectin meant for horse parasite treatment … because they can obtain it easier than getting a script from their doctor.

The media love reporting these crackpot theories as they work on all elements of the audience. The gullible take it as something worthy of their attention, and everyone else finds it a mix of comedy and tragedy. But how much traction is Ivermectin really getting. Let’s look at the data.

Two months ago searches around the term really started to spike, rising around 800%. And Google predicts this will continue rising.

In comparison to vaccine, the demand around Ivermectin information is still narrow. Right now, there are 10x the searches for ‘vaccine’ as there are for ‘ivermectin’

Australia’s United Australia Party, which is running front page ads across the majority of Australian newspapers as a recruitment tool to push its controversial views onto new and gullible Australian’s, believes Ivermectin is worthy of more focus.

And Australia isn’t immune from the hysteria around this crazy concept. Look at the Google search data below. Ivermectin is up 10x over the past 3 months.

The good news is right now there is 46x the demand for ‘vaccine’ information than there is for ‘Ivermectin’. This is much better than the ratio in the United States (however we are at a very different place when it comes to vaccine administration)

What it does show is that fringe theories can explode very quickly, especially when they have a media push behind them and appeal to the noisy and paranoid fringes of the social web.

New Afterpay research data from Alphabeta/Accenture shows plenty of growth in BNPL

Afterpay commissioned Alphabeta to conduct a bunch of research around the sector, and it was published last week. I recommend you take a read.

Domestically Afterpay is the best indicator of the health of the BNPL sector. And this is a sector in rude health. It’s growing at a rapid pace and is upending an entire category in the process.

My fascination with BNPL is due to it feeling more like a customer acquisition channel like a Google or Facebook than a payment pipe. I am also fascinated by it as it’s a disruptive product that has the opportunity to be disrupted by the incumbents. For instance, Paypal is offering pay in 4 now. And with its integration into basically every retailer in the world, plus its huge customer base, it creates a compelling alternative for those already in category, and an easy addition for those new to the category.

Three pieces of data from the report really captured my interest.

Firstly, since COVID emerged BNPL has exploded. The data suggests it’s up 120% since COVID began. For the same period credit is flat, and debit is up 20%.

Secondly, the report outlines that BNPL only accounts for 5% of total retail spend. Now - this excludes cafes, restaurants and food takeaway … but seems to include grocery. This suggests there’s plenty of growth for the BNPL mechanic, especially as the main providers begin to offer products which are as easy to use in physical locations as they are in ecom.

Lastly, BNPL isn’t just a young person thing. BNPL is up more than 2x across Gen Z, Millennials and Gen X. Debit is also up across both of these 3 cohorts. My view is there is huge growth potential in Gen X usage of BNPL, driven by higher ticket price purchases like consumer electronics and appliances.

Afterpay launches Ads. Retail media keeps getting more competitive

Afterpay has launched in-app advertising, launching a promoted post ad unit with sponsored deals and collections within its mobile app.

This is a smart move, as it allows Afterpay merchants to use the app to promote new collections, specials and deals to the vast Afterpay audience.

It follows moves by retailers globally to start charging for prominent position within owned real estate, and is more an extension of the well known tactic of in-store media than a brand new approach.

The Afterpay offering will be compelling to its retailer merchants as it has the ability to utilise location, spending habits, demographics and interests to tailor targeting and messaging. Afterpay knows a lot about how its users shop, browse and research … and this ad product is the first step in what is likely a concerted effort to commercialise this insight.

For media companies with a high reliance on retail clients, this represents another threat competing for ad revenue. My view is that in a low growth ad market, one ad products success is ultimately at the expense of another ad product. So for Afterpay ads, who is likely to feel the effects?

When is Australia likely to re-open? Some thinking around 3 possible scenarios.

Right now this is probably the question most of us really want answered. And it's a tough one to answer as we don't have a huge amount of precedent to go off.

I decided to run some scenarios based on the data I've been analysing. It's important to note I don't have any formal statistical qualifications and most of the work I do around data is related to either financial information or marketing performance. So take these predictions with a grain of salt.

Also, given that some vaccines have been approved by ATAGI to be administered to 12-15 year olds (in addition to 16+), I have extended the 80% double vaxxed threshold to 12+ population. If we are going to vaccination 12-15 year olds, and include these in the numbers, then we cannot continue to base opening on 16+ (in my opinion).

Lastly, these predictions are made on vaccines administered and do not factor in case numbers. I'm a strategy guy, not a medicine one.

The Super bullish scenario - 80% threshold hit in mid November 2021.

This scenario implies that the volume of vaccines (2.2m) administered last week (w/e 28/8) continues all the way through at a constant rate into November. It also implies a 2 week gap between when 80% are double jabbed, and waiting 2 weeks for the second vaccine to properly kick in. It also implies there are no supply issues, no distribution issues etc.

My view is this is likely too optimistic. Remember, the 80% threshold is of 12+, not 16+, which is 21.8 people. By my calculations, 80% of 12+ represents approximately 70% of the TOTAL population. It basically implies a straight line appetite for vaccination across all areas, all demographics, all ages and no slowing whatsoever in volume.

The cautiously optimistic scenario - 80% threshold hit in mid December 2021

This scenario implies that between now the 80% figure, average vaccines administered by week are equal to the average of the past 8 weeks. What this basically assumes is right now we are at the peak of weekly vaccines administered, and the next 8+ weeks will gradually drop at the same level that past 8 weeks rose. Basically a bell curve. This scenario also implies 2 week wait for the 2nd vaccine to take effect.

Given the differences in vaccine uptake by geographies, this feels like a more likely scenario in terms of getting the nation to 80% 12+, but not having geographical areas (particularly in QLD and WA significantly below the opening threshold) left behind.

If I was a betting man (which I'm not) - this would be the scenario I'd be leaning towards.

The bearish scenario - 80% threshold hit in mid March 2022.

This scenario implies vaccination over the next 5 months starts to slow, and starts to represent a decrease in this time that is equal to the increase we have seen over the past 5 months. It implies that as the highly vaccinated areas that are pushing ahead above the national average (think Sydney metro area, parts of Melbourne, regional VIC and TAS) hit 80%, the lower vaccinated areas currently sitting under the national average (think QLD regional, WA regional, parts of SA metro) continue to move at a reduced speed.

This scenario implies significant challenges in terms of 'mopping up' the vaccine hesitant after those who are pro vaccine have been vaccinated. It's less an issue of vaccine resistant/anti vaccine numbers being the blocker. This scenario also implied the same distribution channels remain, and state and federal governments don't change approaches to target areas that are below the national average.

As the name implies, it's the bearish scenario.

The March quarter of 2022 is shaping up to be a big one.

I’ve been thinking a lot about where the ad market will end 2021 and start 2022, and my view is largely an optimistic one.

This is probably something I’ll explore more next week, but the main factors influencing this are:

the latest a federal election can be held is May 2022. 21 May to be exact. With 6 weeks notice this would mean that it would be announced early April. My view is an election is likely to fall between the beginning of March and the end of April. Which means campaigning will fall either way into the March quarter, and there will likely be some reasonable federal government ad spend in market before this (if history is any indication). Election time equals new money into market.

My relatively uninformed view is we won’t ‘reopen’ before mid December. This is explained above. This means physical retail will remain challenged for the majority of the December quarter and it’s unlikely to see a lift from the same period in 2020. On top of this, the good times/bad times index from the Roy Morgan consumer confidence index is still very much skewing towards ‘bad times’ … which suggests to me people will be unlikely to dent their savings until they feel a bit more optimistic about the reopening.

This means the March 2022 quarter will likely see high levels of optimism post hitting vaccine targets, a reasonable amount of banked savings looking for discretionary products to be used on, pre election government feel good advertising, and then a hotly contested election where advertising will play a large role. It may also coincide with increased advertising from the travel industry - especially if selected international destinations become feasible options for holidays or business travel.

My view right now is the December quarter will likely be flat on the whole, but the March quarter will be significantly up for TV, out of home and digital.

To finish …

Read this - Benedict Evans on privacy, ads and confusion. An interesting read from one of the best analysts on media and technology.

Watch this - Billions returns on September 6 on Stan. After a years absence we need this over the top drama back in our lives.

Donate to this - UNHCR for Afghanistan.