The Commercial Experience 21.01

The Commercial Experience 21.01

Welcome to The Commercial Experience newsletter

Hi everyone,

Welcome to the first edition of The Commercial Experience.

A bit about this newsletter

The idea for TCE is to provide analysis and perspective on issues that occur at the intersection of 3 areas - media, technology and commerce.

Ideally every thing covered within is operating across two or more of these areas. It’s these intersections and overlaps that I find most interesting, and I hope you do as well.

TCE will be dispatched every Wednesday morning in the AM. And you’ll be able to view it in your inbox, or on the Substack domain.

I’m a huge fan of newsletters such as Axios Media Trends, CB Insights, Stratechery, CNN Reliable Sources and Mumbrella Best of The Week, and will happily be borrowing/stealing inspiration from how they present topical and timely information. It will sometimes have an Australian bent, and other times will look at global issues that are relevant to the Australian market. At this stage 80-90% of the audience is Australian so the idea is to focus on what is relevant to them.

Formalities done. Let’s get to it.

Intersection 1: Consumer Confidence and the 2021 CY Q4 ad market

Writing this in the middle of a lockdown, in a city under curfew, it’s hard not to have COVID and the current situation front of mind.

Local media companies have reported, since March of 2021, very strong year on year improvements as they bounce from COVID. It’s been a strong turnaround, and a sign that business was returning to normal. A ‘new’ normal, but one that felt very much like the old one.

The consensus was the momentum would roar all the way to Christmas, driven by a strong September quarter. For all intents and purposes, you can assume the September quarter is right now finalised, and you can assume it’ll be another low double digit year on year increase. Even though Sydney is in the grip of a huge case blowout, Melbourne is under curfew and in total 12 million Australians are living under lockdown, the money for the quarter has been allocated and is unlikely to be backed out.

However, the December quarter is looking a lot more shaky. The reason? Consumer confidence has plummeted.

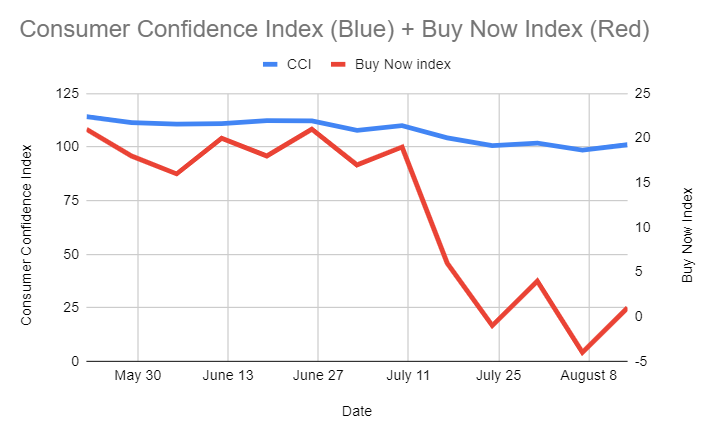

Below I have plotted the ANZ Roy Morgan Consumer Confidence Index since the end of May. That’s the blue line. It’s down around 10-12% in that time. This is a red flag.

In the red I’ve plotted what I’ve called the ‘Buy Now’ index. It’s a metric based on the question in the consumer confidence survey asking respondents to answers yes or no as to whether now is a good time to buy major household purchases. That’s gone from a net +21 to a net -5. The most recent report puts it at 0. This means the same amount of respondents below now is a bad time to buy as those who think it’s a good time.

Why does this concern me? Well, it may suggest people are closing their wallets as they’re now unsure what the immediate future may hold. This metric, in my view, is one that is very closely linked to short term discretionary spend and one that has the potential to impact sectors such as retail, automotive, financial services, travel and technology.

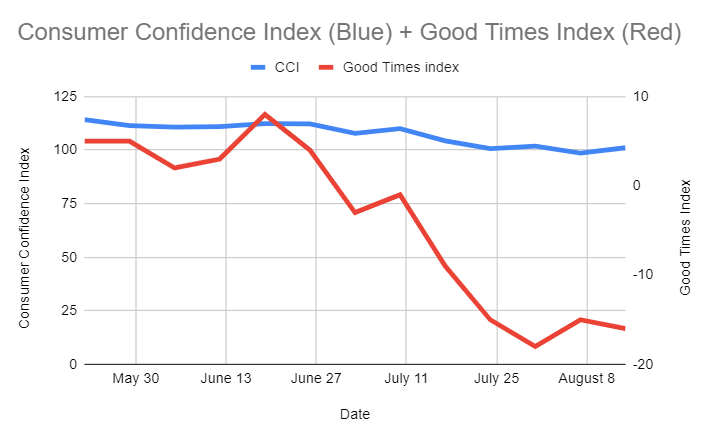

The second metric that is also a red flag is what I’ve coined the ‘Good Times Index’ - this is the number of respondents who believe we as a nation will have good times, or bad times, over the next 12 months. When consumer confidence fell in a hole when COVID hit, it was this question which drove it. People on the whole saw bad times ahead. As we were told that COVID was under control and that Australia had weathered the storm, this figure started to recover, and from February of 2021 was trending as a positive number. From mid June it has plummeted, and is now at the lowest levels since October 2020.

Remember, these figures were compiled before Victoria went into curfew and had its lockdown extended, and before NSW saw case loads in the mid 400’s. It’s likely over the next 2-3 weeks this will continue to drop. These two metrics - good times and buy now - are trending the wrong way to suggest that the December quarter will perform at levels above the year prior. Australia is a different place - less optimistic, more restricted, more locked down, and more unsure of what’s to come.

Intersection 2: Seven West Full Year Results highlight 3 areas for optimism, and one big question around diversification

The Seven West Media figures reported this week showed a network that has definitely improved under CEO James Warburton.

The big 3 areas for me

revenue was up 6.2%

Costs were down 6.4%

Debt continues to drop

The share market punished Seven on Tuesday, with the share price dropping 9.47% - which is more likely an reaction to the likelihood of a flat December quarter due to the COVID related predicament Australian finds itself in, rather than an observation on Seven itself.

With Seven showing positive signs, it’s worth looking at where it decides to look for expansion. The obvious area is SVOD, and the obvious approach is for Seven to try and use advertising inventory instead of cash (or at best, a mix of cash and advertising value) to find a way to take an equity stake in a local SVOD provider (such as Streamotion), or an international player (such as Peacock).

One area I think Seven, and most of the local media companies, should look at more closely is using ad inventory as a way of taking equity in a pureplay ecommerce business that has the ability to appeal to a mass audience and grow quickly off the back of TV advertising. Think of an appliances retailer, furniture (like a Temple and Webster type business), or beauty (similar to an Adore Beauty). This is a good way to use advertising inventory to deliver a high grow return to shareholders. For the ecommerce business it provides access to millions of loungerooms. The ability to play alongside the global commerce businesses that continue to invest so much in TV.

Generally this approach has been viewed with caution as no local media business has wanted to be seen to compete with its largest clients. Retail, beauty, homewares - these are lucrative categories for TV. However many of these businesses, such as Woolworths through Cartology, Coles/Wesfarmers via FlyBuys, are now competing directly with the networks for ad dollars. One could argue businesses like Quantium - which works with Woolworths and another big advertisers, Commbank, is also doing the same. Even Samsung is, with Samsung Ads across Connected TV.

It’s a good time right now to think about whether a local media business wants to miss out on these ecommerce opportunities, or whether it wants to operate more at the intersection of audience and commerce rather than just audience and content. Seven is the least diversified of the large local media companies, and one that would have the most to gain.

Intersection 3: The rise and rise (and rise) of Google, Facebook, Snapchat and Twitter and what it tells us about the link between media and commerce.

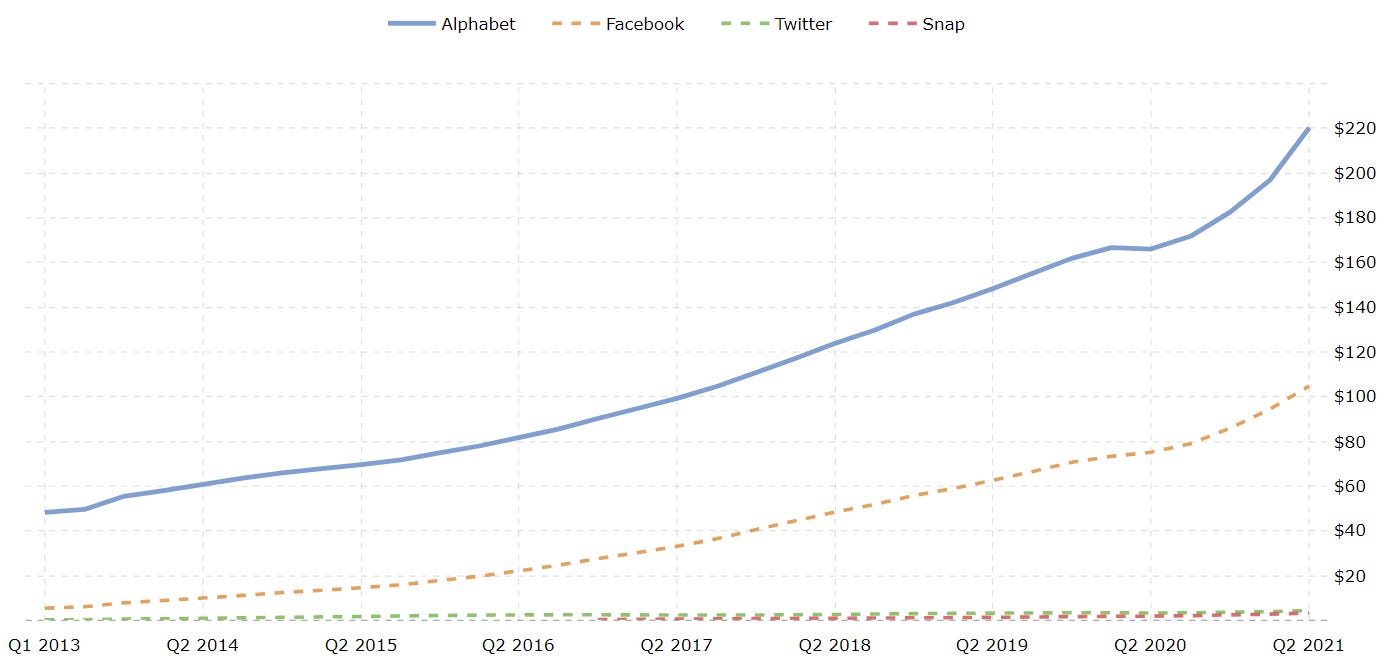

Take a look at this graph. It plots the rolling 12 month revenue of four of the biggest digital media platforms.

Sure, it demonstrates that Google and Facebook command the lions share of the market. And it shows these companies have enjoyed seemingly endless periods of growth over the last decade (and more). But what it shows is just how much money these four businesses have hoovered up over the last year from the ad market.

New money. A staggering incremental $86B USD across 12 months. In the middle of a pandemic and ruined advertising market.

For the 12 months ending June 30 2021, these businesses generated $86B USD more than they did for the year prior.

To put this in perspective, the largest US pureplay TV/entertainment company ViacomCBS (owners of Ten in Australia), generated $26B USD for the entire year. Seven West Media here in Australia generated $1.28B AUD for the year.

Thinking of these businesses as advertising businesses is short sighted. Yes, they sell advertising and have advertising sales platforms. But for most of their customers, they are a customer delivery pipeline as opposed to the more traditional media companies they compete with. These platforms have highly tuned software which is optimised to drive commerce, drive purchases, and drive consumption.

Their customers view them just like I view petrol for my car - as an essential resource to help me reach my destination. I would go as far as to say they are now a non discretionary marketing purchase.

The reason is they have focused so heavily on driving immediate and easy to quantify commercial outcomes that they will start to compete with retail shopping centre and land owners more than traditional media companies as they grow over the next decade.

And their $86B in new money in just 12 months shows the spoils that can be had when commerce and media are closely linked.

Some things you should do

Watch this - Untold - Malice At The Palace - Netflix

Read this - Chloe Hooper - Going Full Circle - Mumbrella

Donate to this -Mirabel Foundation - They care for children orphaned due to drug abuse

Until next week,

Ben

This is wonderful analysis. Thanks Ben.